We are just one month into 2021 and already it feels as if things have started off on the wrong foot. Several countries / cities have re-declared state of emergencies and re-imposed lockdowns due to the virus, the distribution of vaccines has not gone as smoothly as expected (which I predicted in my previous post), oh, and for the first time in nearly 207 years, the United States Capitol was overrun… On January 6, 2021, a mob of Trump supporters stormed the Capitol Building and disrupted a joint session of Congress that was in the middle of certifying President Elect Biden’s victory in the 2020 election. Some have called this an act of “domestic terrorism” or “insurrection.” What we can say with full certainty is the last time the United States Capitol was overrun dates back to 1814 when the British Army sacked the Capitol during the War of 1812.

Do you know what else dates back to the 19th century? The publication of Charles Mackay’s “Extraordinary Popular Delusions and the Madness of Crowds” in 1841. Over the past month, I spent some time re-reading this classic and the lessons contained within are just as relevant today. The first three chapters of Mackay’s seminal work focuses on economic bubbles. Chapter 1 is about the Mississippi Company bubble of 1719–1720, Chapter 2 highlights the South Sea Company bubble of 1711–1720, and Chapter 3 focuses on the Dutch tulip mania of the early 17th century. What could these three episodes dating back 300+ years (almost 400 years in the case of the Dutch tulip mania) possibly have to do with 2021?

Quite a bit, in fact.

The long bull market that we have experienced in the aftermath of the Great Recession has now evolved into an undeniable bubble of spectacular proportions. The “Warren Buffet indicator” (the ratio of total stock market capitalization to GDP) is about 190% (well above the record high of ~143% at the peak of the dot-com bubble in March 2000) There have been 480 IPOs in 2020 and more than half that number (248) in backdoor listings through Special Purpose Acquisition Companies (SPAC). Due in part to services such as Robinhood, the volume of small retail purchases (less than 10 contracts) of call options on US equities has increased 8X compared to 2019 levels.

Speaking of small retail purchases and Robinhood, a community of retail traders on the online discussion forum Reddit have recently received widespread national media attention after their trading activities caused shares of the struggling brick & mortar video game retailer GameStop (ticker: GME) to soar from less than $20 a share at the beginning of January to a high of $483 a share on January 28 at 10:01 AM (Sidenote: You can retrieve such precise stock market data from Alpha Vantage), causing investors who were short the stock (betting that the stock would decrease in price) such as Citron Research and Melvin Capital to incur massive losses. Many of these retail investors used Robinhood’s “free” brokerage app to buy GME stock.

I use the words “free” in quotation marks because the service is not really “free,” much in the way services such as Facebook are not really free. Yes, it is free for Robinhood users to buy and sell shares or options on the app, but the reason behind that is because Robinhood users are not actually the “customer” but are in reality the “product.” The outspoken venture capitalist Chamath Palihapitiya – who incidentally was an early employee at Facebook who led the team at Facebook that created features designed to systematically increase the addictiveness of Facebook grew the user base from 90 million (the level at which Facebook’s user base was stagnating at the time) to a path towards 1 billion by the time he left – recently put out a tweet describing as such:

Facebook and @RobinhoodApp are the same:

They both trick you into thinking you are the customer. But, in fact, you are the product and your data is the asset.

These assets are then sold to their true customers who pay them money and always at your expense.

STOP BEING TRICKED!

— Chamath Palihapitiya (@chamath) January 29, 2021

In an unprecedented move, Robinhood and a select number of brokerage firms on Jan 28, 2021 disabled the ability for its users to buy shares of GameStop and a few other companies (it was still possible to sell), which caused the price of these securities to crash over 44%. The official stance of Robinhood and these other brokerage firms is that this was done due to capital and regulatory requirements, but there is strong evidence to suggest the real reason was to allow stakeholders on the wrong side of the bet such as Citadel (which is Robinhood’s largest actual customer, accounting for hundreds of millions in revenue to Robinhood each year), Point72 Asset Management, and Melvin Capital (Citadel and Point72 collectively invested $2.75 billion in an emergency influx of cash to stabilize Melvin Capital) to regroup and get a respite from the unrelenting short squeeze.

As a neutral observer of this all (I have never owned any GameStop stock or any of the stocks that have been part of this recent phenomenon), I’ve had two thoughts: One, it is an unfortunate reality of the world that we live in that there exists two different sets of rules. One set of rules for the rich and another set of rules for everyone else; Two, as someone with a significant portion of my net worth tied to the stock of publicly traded companies, these recent events have dismayed me at how corrupted our capital markets have become from their original purpose.

Well functioning capital markets are absolutely essential for a modern economy as they allow businesses that need capital to be connected with those who have capital to invest. Businesses that have capital are able to use it to grow which (hopefully!) results in the creation of new jobs, innovation, and prosperity. Unfortunately, capital markets today have devolved into something similar to a casino in which gamblers speculators are engaged in zero-sum games that create incredible fortunes for the few winners but very little of value created for the rest of society.

A friend from grad school asked the other day in a mutual chat group that we share if any of us were participating in this stock run-up, and my answer was unapologetically “no” — my investments are mostly in no-thrills Vanguard index funds with a few individual names here and there.

While it is still too early to tell how this will turn out, it is impossible not to draw parallels between this current mania and the extraordinary manias described in Mackay’s book. In the short-term, Robinhood is facing multiple class-action lawsuits and lawmakers from both sides of the aisle have taken notice.

This is unacceptable.

We now need to know more about @RobinhoodApp’s decision to block retail investors from purchasing stock while hedge funds are freely able to trade the stock as they see fit.

As a member of the Financial Services Cmte, I’d support a hearing if necessary. https://t.co/4Qyrolgzyt

— Alexandria Ocasio-Cortez (@AOC) January 28, 2021

Many people draw similarities with this current bubble to the dotcom bubble at the turn of the century, but there is a key difference. Back in 1999-2000, the 10-Year US Treasury yields were at 6%. It is also worth mentioning that Nobel laureate Robert Shiller – who correctly called the 2000 and 2007 bubbles – is hedging his bets this time, recently making the point that his iconic cyclically adjusted price-to-earnings (CAPE) ratio (which suggests stocks are nearly as overpriced as they were at the peak of the dot com bubble) shows that stocks are not overvalued given where interest rates are. Shiller’s new excess CAPE yield (ECY), which is the inverse of the CAPE ratio (33.8 as of 1/29/2021) or approximately 3.0%, minus the interest rate on 10-Year Treasury Inflation-Indexed Security Rate of -1%, results in a excess CAPE yield of 4.0%, indicating that equities are more attractive than bonds yielding 1% or less in nominal terms.

Another important difference between this bubble and previous bubbles is the strength (or rather the perceived strength) of the economy. Previous bubbles have combined expansionary monetary policy with economic conditions that are perceived at the time, rightly or wrongly, to be favorable and extrapolated to remain indefinitely so in the future. Today’s economy is starkly different: only partially recovered, with reasonably high expectations of an eventual slowdown, and most definitely facing high levels of uncertainty, and yet the market today is at a much higher point today than it was last fall when the economy was seemingly doing just fine and the unemployment rate was at historic lows.

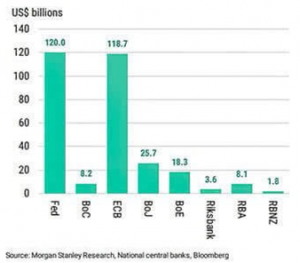

It certainly feels that this time, more than in any previous bubble, investors are relying on favorable monetary conditions and zero interest rates extrapolated indefinitely. The problem is that it is impossible for such conditions to last forever, for as in physics, for every action, there is an equal and opposite reaction. When central banks expand the money supply, that money has to go somewhere. Since 2008, that money inflated asset prices of the wealthiest class, which is why stocks, luxury goods, and rare artwork have seen such dramatic increases in their prices.

If you believe the numbers released by CPI, it may appear that there hasn’t been much inflation in the “real economy” – but as one of my favorite sci-fi writers William Gibson says, “The future is already here, it’s just not very evenly distributed.” In a similar vein, inflation is “already here, it’s just not evenly distributed.” One need look no further than the prices of education, housing, and medical care over the past decades, which increased at rates far above the rate of inflation.

Moreover, prices are going up because the money supply is expanding at a rate far higher than growth in the actual economy. The S&P 500 is already at unprecedented high levels, but it could very easily continue to climb higher because of accommodative monetary conditions and endless money printing. Stocks like Tesla and now GameStop, which have completely defied all logic, could continue to rise in price since fundamentals and reality are essentially decoupled in a bubble.

What will cause an end to this madness? As I’ve already said, accommodative monetary conditions and zero interest rates cannot last forever. At some point, rates will have to increase. It could be some kind of major geo-political event such as war, or perhaps a change in the reserve currency, being blindsided by another health crisis (this time with a disease that is much more deadly than covid-19). If that does not seem plausible, just remember that it was not too long ago when it was conventional wisdom to believe that interest rates would stay high forever and shares in the common stock of corporations were consider at best speculative investments, and at worst poor investments.

The great Yogi Berra once said, most likely apocryphally, that “It’s tough to make predictions, especially about the future.” I will not hazard a prediction when rates will eventually rise or some other event that changes the current investing environment, but I am absolutely convinced this bubble will go down in financial history as one of the greatest bubbles of all time ranking right up there with the South Sea bubble, the Great Crash of 1929, and the more recent ones over the past two decades. As they say in the language of my forefathers: Plus ça change, plus c’est la même chose.

—JOP