Via the Big Picture and Paul Kedrosky (again), a frightening view of the potential depths of the sub-prime crisis, still unfolding:

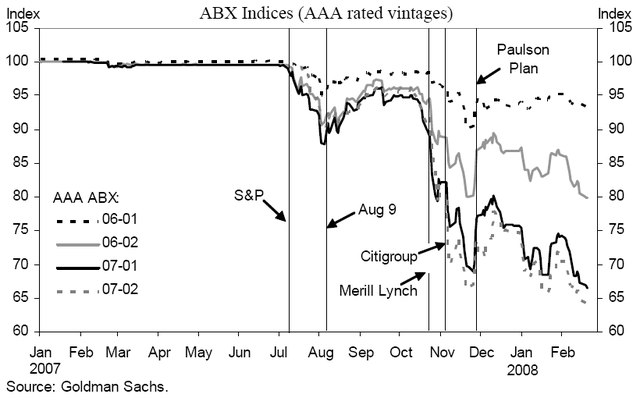

This report discusses the implications of the recent financial market turmoil for central banks. We start by characterizing the disruptions in the financial markets and compare these dislocations to previous periods of financial stress. We confirm the conventional view that the current problems in financial markets are concentrated in institutions that have exposure to mortgage securities. We use several methods to estimate the ultimate losses on these securities. Our best (very uncertain) guess is that the losses will total about $400 billion, with about half being borne by leveraged U.S. financial institutions. We then highlight the role of leverage and mark-to-market accounting in propagating this shock. This perspective implies an estimate of the eventual contraction in balance sheets of these institutions, which will include a substantial reduction in credit to businesses and households. We close by exploring the feedback from credit availability to the broader economy and provide new evidence that contractions in financial institutions balance sheets’ cause a reduction in real GDP growth.

Leveraged Losses: Lessons from the Mortgage Market Meltdowns [.pdf] by David Greenlaw of Morgan Stanley, Jan Hatzius of Goldman Sachs, Anil Kashyap of the University of Chicago and Hyun Song Shin of Princeton University.

They’re talking, in total, about two trillion dollars and 1.5% of GDP!